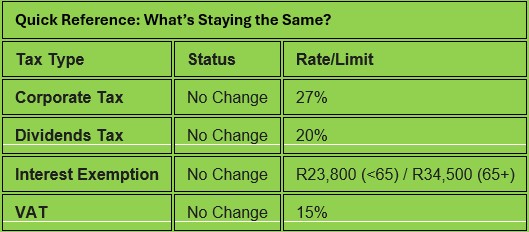

What Investors Need to Know About the Latest Tax Tweaks

The 2026 South African Budget is officially out, and while there weren’t any “earth-shaking” changes to the major tax rates, there are several “bracket creep” adjustments and threshold increases that should put a little extra wind in the sails of savvy investors and savers.

If you’ve been waiting for a reason to top up your retirement fund or re-evaluate your property holdings, today’s news might just give you that nudge. Here is the lowdown on the highlights and what they mean for your wallet.

1. A Boost for Your Tax-Free Savings

The headline for many individual investors is the first increase to the Tax-Free Savings Account (TFSA) annual contribution limit since 2021.

- The Change: The annual limit is jumping from R36,000 to R46,000 starting 1 March 2026.

- The Catch: The lifetime limit stays firmly at R500,000.

- The Investor Takeaway: If you can afford the higher monthly contribution, you’ll reach that R500,000 lifetime ceiling faster, allowing more of your compound growth to happen within a tax-free bubble sooner.

2. Retirement Fund Wins

National Treasury is giving you a bit more room to breathe when it comes to retirement planning.

- Higher Deductions: The cap on tax-deductible contributions to pension, provident, or RA funds is increasing from R350,000 to R430,000 per year. The 27.5% of taxable income limit still applies.

- Lump Sum Flexibility: If you have a small retirement “pot,” the de minimis limit for annuitization is rising from R247,500 to R360,000. This means if your total interest is below this amount at retirement, you can take the whole thing as a lump sum instead of being forced to buy an annuity.

3. Capital Gains and Property

Good news if you are planning to sell your home or a small business:

- Primary Residence: The capital gains tax (CGT) exclusion on the disposal of your primary home is increasing from R2 million to R3 million.

- Annual Exclusion: The general annual CGT exclusion for individuals and special trusts moves from R40,000 to R50,000.

- Small Business Owners: If you’re over 55 and selling your business, the exclusion on capital gains is being bumped up to R2.7 million (from R1.8 million), provided the business’s market value doesn’t exceed R15 million.

4. The “Spouse Loophole” is Closing

Treasury has noticed some “creative” tax planning where one spouse ceases tax residency before the other to move assets tax-free.

Effective 25 February 2026, the donations tax exemption between spouses will only apply if the recipient spouse is a South African resident. If your spouse has already “emigrated” for tax purposes, donations to them may now trigger a 20% tax.

Your Next Steps

- Adjust your Debit Orders: If you have a TFSA, consider increasing your monthly contribution to hit that new R46,000 annual limit.

- Maximize your RA: If you are a high-earner, check if you can contribute more to your retirement fund to take advantage of the new R430,000 deduction ceiling.

- Review Global Assets: If you or your spouse are considering moving abroad, chat with a tax professional immediately about the new restrictions on inter-spousal donations.